Larry S. Harris, Jr.

Mortgage Broker

[email protected]

NMLS# 2599571

We are a full-service mortgage brokerage dedicated to guiding clients through every stage of the home financing journey with expertise and care

I HAVE 30+ YEARS OF EXPERIENCE

The Best Way To Find Your Perfect Home

Start with the right tools, expert guidance, and a clear plan — and we’ve got you covered.

Assess your home-buying goals

Provide personalized advice to meet your goals

Review your finances, income, and credit

Provide you with loan options tailored to you

Navigate each step of the home-buying journey

Work with internal APM teams to get your loan all the way through to approval, closing, and keys in hand

I will be there through it all, leaving you with ample time to find your dream home as we guide you to a successful, speedy, and hassle-free closing.

About Us

At LSH Home Loans, we specialize in guiding homebuyers, homeowners, and investors through seamless financing solutions. With deep industry expertise and a client-first mindset, we make securing the right mortgage simple, transparent, and stress-free.

Services

The Best Way To Find Your Perfect Home

Conventional

A home loan that falls under the conforming loan limit of $726,000, and can be as high as $1,089,300 in high cost area, which is set annually by the Federal Housing Finance Agency. The interest rate is fixed and the loan term is typically 15 or 30 years.

Best for: People with down payments or equity

Jumbo

Multiple jumbo options exist if you need a home loan that exceeds the current confirming limit for higher-priced real restate markets.

Fixed or adjustable rates, Credit score of 700 or higher often required, and a minimum 10% down often required.

Best for: Buyers of higher-priced homes

VA

Backed by the Department of Veterans Affairs. Veterans, active-duty service members, and surviving spouses with qualifying income and credit can buy a primary residence with favorable terms with no downpayment, upfront VA fee required, and no mortgage insurance

Best for: Military-qualified borrowers

FHA

Loans are backed by the Federal Housing Administration and are designed to help lower-income borrowers buy a home.

Down payment as low as 3.5%, credit score are low as 600, mortgage insurance premium payments required

Best for: Borrowers who need a little more help qualifying

USDA

Are backed or issued by the U.S. Department of Agriculture. Your small-town dreams of rural homeownership can be made possible with a USDA home loan.

No downpayment required on most properties, home improvement loans and grant options, income limits and property value caps apply

Best for: Income-qualified buyers in rural and some suburban areas who want a low or zero downpayment

Specialty

Loan programs that accommodate specific and unique needs, such as self-employed borrowers who have trouble showing their income or property types that are outside the norm.

Best for: Borrowers who have unique qualifying or property needs

The Best Way To Find Your Perfect Home

Conventional

A home loan that falls under the conforming loan limit of $726,000, and can be as high as $1,089,300 in high cost area, which is set annually by the Federal Housing Finance Agency. The interest rate is fixed and the loan term is typically 15 or 30 years.

Best for: People with down payments or equity

Jumbo

Multiple jumbo options exist if you need a home loan that exceeds the currrent confirming limit for higher-priced real restate markets.

Fixed or adjustable rates, Credit score of 700 or higher often required, and a minimum 10% down often required.

Best for: Buyers of higher-priced homes

VA

Backed by the Department of Veterans Affairs. Veterans, active-duty service members, and surviving spouses with qualifying income and credit can buy a primary residence with favorable terms with no downpayment, upfront VA fee required, and no mortgage insurance

Best for: Military-qualified borrowers

FHA

Loans are backed by the Federal Housing Administration and are designed to help lower-income borrowers buy a home.

Down payment as low as 3.5%, credit score are low as 600, mortgage insurance premium payments required

Best for: Borrowers who need a little more help qualifying

USDA

Are backed or issued by the U.S. Department of Agriculture. Your small-town dreams of rural homeownership can be made possible with a USDA home loan.

No downpayment required on most properties, home improvement loans and grant options, income limits and property value caps apply

Best for: Income-qualified buyers in rural and some suburban areas who want a low or zero downpayment

Specialty

Loan programs that accommodate specific and unique needs, such as self-employed borrowers who have trouble showing their income or property types that are outside the norm.

Best for: Borrowers who have unique qualifying or property needs

Let’s make it official!

Book an appointment, and we’ll dive right in

Ready to turn your dream of owning a home a reality?

Let’s take the stress out of the process and make your first home everything you’ve imagined — and more!

Loan Calculator

Leading the market with a

client-first focus

Get in touch

Receive expert guidance to maximize your next purchase, sale, or investment.

2361 DeKalb Medical Pkwy Suite 101, Lithonia, Georgia, 30058

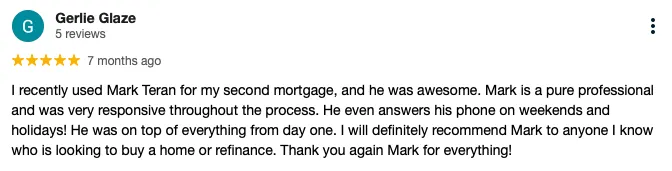

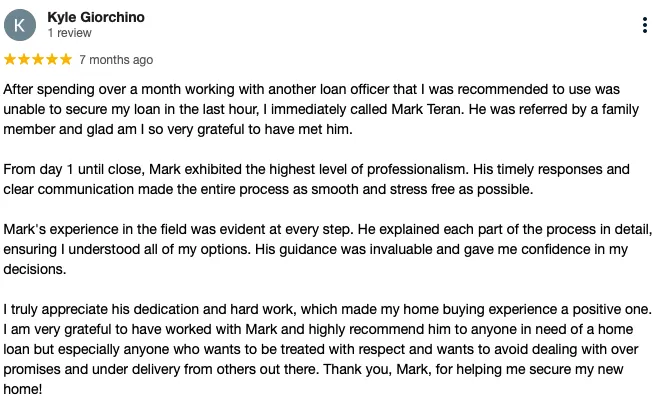

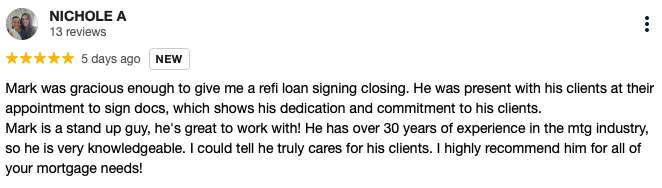

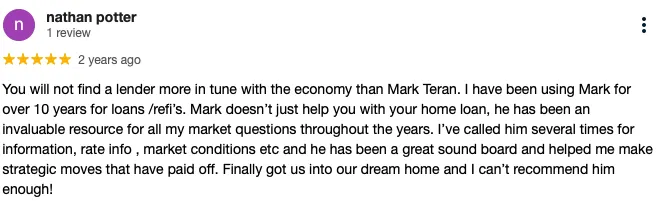

What others are saying